A structural decline in the rate of house sales means the average turnover of a property has almost trebled since the 1980s from eight to 23 years, according to a new report by the Intermediary Mortgage Lenders Association (IMLA).

The second annual report from IMLA – The new ‘normal’ one year on: is the march back to a sustainable market on track? – examines trends in the mortgage and housing markets in order to assess the strength of the post-recession recovery.

It shows annual turnover of the private housing stock fell from over 12% to 4.5% over the last three decades. As a result, IMLA’s analysis indicates the ‘average’ home currently changes hands once every 23 years compared with every eight years during the 1980s.

The IMLA report argues that low housing turnover is driven by a combination of people buying their first homes later; by a larger private rented sector where turnover is lower; and by the baby boomer ‘hoarding effect’ where middle-aged homeowners are staying put, tying up a large part of the housing stock. These factors are likely to keep turnover down for the foreseeable future, potentially limiting mortgage lending and restricting access to existing properties.

IMLA’s analysis also shows the estimated contribution of mortgage finance to the total value of UK housing transactions hit a new all-time low of 41.7% last year. It means just £4.17 of every £10 spent on house purchases in 2014 was funded by mortgages while cash or equity made up £5.83 (58.3%).

Despite forecasting a slight increase in gross mortgage lending over the next two years, IMLA expects the estimated contribution of cash (including deposits and cash purchases) to housing transactions will exceed 60% for the first time on record by 2016.

Peter Williams, Executive Director for IMLA, commented:

“These figures paint a picture of a housing market where turnover has drastically slowed in the last thirty years. Quite simply, in the absence of a sustained rise in housebuilding and improved affordability and turnover, the fact that properties are coming onto the market less frequently severely limits the scope for would-be first time buyers to graduate to owning their own homes.”

“Inertia in the property market spells danger for future owner-occupation levels, and the growing influence of cash and equity is sowing the seeds of a permanent social divide. Having said that, we will see some continued growth in mortgage lending – and as the market stabilises and wages rise, we may also start to see affordability improving.”

Brokers, building societies and specialist lenders benefitting under MMR

IMLA’s report also assesses how the mortgage market recovery has been tempered in the last year by worsened housing affordability and tighter lending restrictions since April’s implementation of the Mortgage Market Review (MMR) and October’s macro-prudential changes prompted by the Financial Policy Committee (FPC).

While gross mortgage lending was running 36% up year-on-year in January 2014, it was down 2% by December and the market softened further in January 2015, falling 8% annually.

The IMLA forecasts offer a cautious expectation of growth in 2015, with strong economic fundamentals – including low inflation, rising incomes and continued low interest rates – balancing these negative influences and supporting a 3% annual rise in gross lending to £210bn.

IMLA’s analysis also shows how brokers, building societies and specialist lenders have benefited most under MMR. The end of non-advised sales has led lenders to source more business from brokers, and between Q1 2014 – immediately before MMR implementation – and Q4 2014 the number of consumers using intermediaries rose by 20% while those going direct to lenders fell 6%.

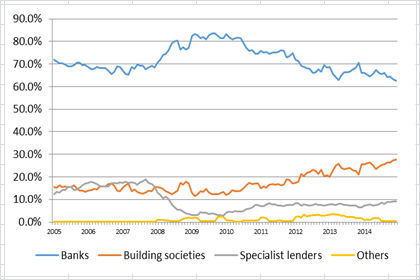

Specialist lenders and building societies are also enjoying a growing share of gross mortgage lending at the expense of banks. Ongoing demand from ‘niche’ borrowers is providing these types of lenders with opportunities to grow, partly because the self-employed and other non-standard customers in the post-MMR world fit less well into the automated loan underwriting systems favoured by some larger lenders.

Chart 1: Share of gross mortgage lending by different types of lender

Peter Williams, Executive Director for IMLA, commented:

“Twelve months ago we took the view that the mortgage market was leaning heavily on temporary support measures while being subject to permanent regulatory changes. The aim of dampening the credit cycle is laudable, but there is a danger that regulation could have an asymmetric effect in the future – curtailing the upswings while providing little support in the downswings.”

“The introduction of the MMR and first use of macro-prudential tools cannot be held entirely responsible for the slowdown over the last year, but we may be getting the first taste of how the new regulatory regime can engineer a more subdued market – even with the policy prop of ultra-low interest rates.”

“Access to advice and products from a broad spectrum of lenders are increasingly vital to borrowers in today’s mortgage market. With more prime borrowers falling into ‘non-standard’ categories, choice is vital so as not to frustrate legitimate applications for mortgage credit.”

For further information please contact:

Rob Thomas, Director of Research, The Wriglesworth Consultancy, 020 7427 1406

Andy Lane / Maham Uzair, The Wriglesworth Consultancy, 020 7427 1400 / Email: imla@wriglesworth.com

Notes to Editors

About IMLA

The Intermediary Mortgage Lenders Association (IMLA) is the trade association that represents mortgage lenders who lend to UK consumers and businesses via the broker channel. Its membership of 52 banks, building societies and specialist lenders include 18 of the 20 largest UK mortgage lenders (measured by gross lending) and account for about 90% of mortgage lending (91.6% of balances and 92.8% of gross lending).

To keep up to date about IMLA in the news, our reports and other announcements, follow us on LinkedIn.