More mortgage borrowers are seeing their applications for mortgage loans given the green light as new products emerge to support ‘non-standard’ circumstances, according to new research by the Intermediary Mortgage Lenders Association (IMLA).

Over a quarter of brokers (26%) reported having no problems sourcing a mortgage for any type of borrower in the second half of 2015, the highest proportion in the post Mortgage Market Review (MMR) era, and a clear sign of improving lending conditions. It represents a significant jump from the proportion of brokers experiencing no problems both in H1 2015 (15%) and H2 2014 (16%).

Some areas beyond the ‘mainstream’ mortgage market have been less well-served since 2008/9, with new regulations introduced to govern lending criteria and fewer products on offer tailored to meet the needs of smaller and less mainstream consumer segments. This includes products to support borrowers seeking lending into retirement, products designed for borrowers with past adverse credit records, and those tailored for self-employed borrowers or those with irregular incomes.

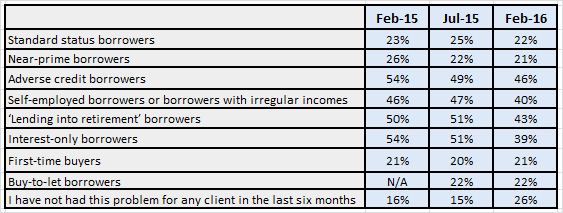

However, IMLA’s research shows fewer brokers are now experiencing problems with sourcing a mortgage for clients in all of these areas, with the most significant improvement seen in sourcing loans for interest-only borrowers. The proportion of brokers having difficulties helping this type of client has fallen 15 percentage points year-on-year to 39%.

Similarly, the proportion of brokers unable to source a mortgage for ‘lending into retirement’ borrowers has dropped seven percentage points to 43%. The picture has also improved for self-employed borrowers, with just 40% of brokers reporting problems over the last six months, down six percentage points from a year ago.

Table 1: Were you unable to source a mortgage for any of the following in the last six months? Percentage of brokers unable to source a mortgage for the following borrowers

The most common circumstances where brokers were unable to source mortgages in H2 2015 continue to be adverse credit (46%), lending into retirement (43%), self-employed borrowers (40%) and interest-only borrowers (39%) – although in each case, the picture has improved.

These product types are becoming increasingly important, in context of the changing UK demographic. More first-time buyers are taking out mortgages with longer terms to spread out their repayments, with 60% now opting for terms that last more than 25 years, meaning more borrowers could be left paying off their debt in retirement.1 Meanwhile the trend towards more working flexibility alongside sluggish wage growth has boosted self-employment levels in the UK, and 15% of the workforce are now self-employed.2

Looking ahead, both lenders and brokers identify first-time buyers as the market area with the best overall growth prospects for 2016, ahead of other segments (homemover, remortgage, buy-to-let, lifetime and further advances). However, when asked about the prospects for product availability, IMLA’s research suggests further improvements could be on their way for other borrower types.

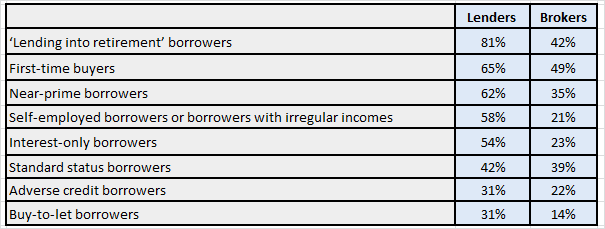

More than half of lenders forecast an improvement in mortgage availability for retirement borrowers, near-prime borrowers, those who are self-employed or with irregular incomes, and interest-only borrowers. In each case, lenders’ confidence exceeds that of brokers.

Table 2: Across the whole market, how do you expect mortgage availability to change for the following types of client in 2016? Percentages are those expecting an improvement

Over half of lenders (54%) reported feeling that mortgage market conditions are currently improving. A total of 68% of lenders and 59% of brokers are confident that gross lending will meet the industry forecast of £237bn for 2016. Additionally, over a quarter of brokers (27%) feel confident lending will exceed this forecast, while more than one in ten (11%) expect 2016 gross lending to exceed the forecast by a significant margin.

1 CML: Affordability bites? Feb 2016

2 Bank of England: “Self-employment: what can we learn from recent developments” 2015 Q1

Peter Williams, Executive Director of IMLA, comments

“If lenders’ expectations are realised, 2016 should see the mortgage market broaden out and start providing greater support to the substantial and still growing non-standard segment of borrowers. Although recent conditions have supported standard homeowners, who are enjoying record low rates and attractive remortgaging options, niche consumers have found it harder to find their feet in the new regulatory landscape. This has been made more difficult by those structural changes triggered by the economic recovery – for example, rising self-employment.

“The FCA has acknowledged this in its call for inputs on mortgage market competition at the end of last year and in its launch of a ‘regulatory sandbox’ to allow the testing of new innovations in a less constrained regulatory environment – to help encourage innovation and new solutions. Lenders, brokers and regulators all have a responsibility in this area to make sure the market adapts and isn’t overly constrained in terms of choice.

“It is, therefore, a very positive step that lenders are expanding their range of products to serve the growing number of non-standard borrowers. This will mean greater choice for the growing segment of borrowers who are self-employed, along with increasing the number of products to support lending into retirement, as well as expanding the options for near-prime borrowers. The survey results offer good news for UK mortgage borrowers and the broker market.”

For further information please contact:

Rob Thomas, Director of Research, Instinctif Partners, 020 7427 1406

Andy Lane / Tora Turton / Maham Uzair / Will Muir, Instinctif Partners, 020 7427 1400

twc.imla@instinctif.com

Notes to Editors

Methodology

The Intermediary Lending Outlook compares views from IMLA members – including senior representatives of banks, building societies and specialist lenders – and 2,450 mortgage intermediaries from across the UK on mortgage market conditions since January 2012.

150 brokers were surveyed independently by Instinctif Partners as part of the latest wave of research in February 2016. IMLA’s membership comprises 30 lenders and accounts for over 70% of mortgage lending via intermediaries.

About IMLA

The Intermediary Mortgage Lenders Association (IMLA) is the trade association that represents mortgage lenders who lend to UK consumers and businesses via the broker channel. Its membership of 52 banks, building societies and specialist lenders include 18 of the 20 largest UK mortgage lenders (measured by gross lending) and account for about 90% of mortgage lending (91.6% of balances and 92.8% of gross lending).

To keep up to date about IMLA in the news, our reports and other announcements, follow us on LinkedIn.